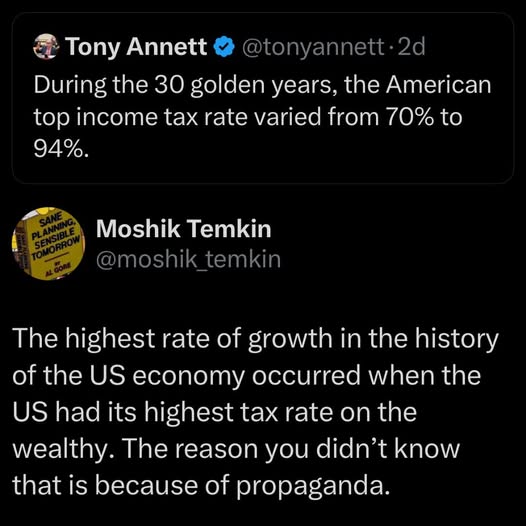

Beyond the glossy images of modern prosperity, a fascinating chapter of American fiscal history reveals that during what many call the “Golden Years,” top income tax rates soared to staggering levels. Recent social media discussions and historical data highlight that over a span of approximately three decades, the highest marginal income tax rate in the United States fluctuated dramatically between 70% and 94%.

This period, encompassing the post-World War II era through the early 1960s, was marked by extraordinary economic growth, yet also by a tax landscape that would be considered unthinkable in today’s context. According to inputs from social media posts by @tonyannett2 and insights from historian Moshik Temkin, during these “30 golden years,” the U.S. government imposed some of the highest income tax rates in its history.

To put this into perspective, today’s top federal income tax rate stands at 37%, a far cry from the historic highs. However, between the 1940s and early 1960s, the federal government levied marginal rates nearing or exceeding 90% for the highest earners. This phenomenon reflected both the economic challenges of the era and a political consensus around robust taxation to fund post-war reconstruction, infrastructure, and social programs.

The race to fund burgeoning government programs was multifaceted. During this period, tax policy was an essential tool to manage income inequality and finance a variety of national initiatives. Notably, the revenue generated from these top rates contributed to the rapid growth of the American middle class, funded the expansion of the highway system, and supported various social safety net programs.

Interestingly, the high rates also prompted debates about fairness and economic incentives. Critics argue that such steep rates could potentially discourage investment and innovation, while proponents believed they were necessary to ensure a fair distribution of wealth and state funding.

Today, as policymakers revisit tax strategies amidst economic uncertainties, understanding the historical levels of taxation provides context to current debates. It also challenges some assumptions about what constitutes “high” or “unsustainable” tax rates. As Moshik Temkin notes, the high rates during the mid-20th centuryare a testament to a different economic philosophy that prioritized societal investment over individual accumulation.

In conclusion, this chapter in America’s fiscal history reminds us that the country has experienced significantly different tax environments. Whether for or against high taxes, knowing this history helps foster a more informed conversation about the role of taxation in shaping the nation’s economic and social fabric.